Money Market vs. Savings Account: What’s the Difference?

February 10, 2025

Money Market vs. Savings Account: What’s the Difference?

One of the most important roles of local and community banks is providing a safe and easy way for customers to save money. Whether they’re saving up for a particular purchase or just setting aside some money as a contingency fund, customers who opt to save money through their banks have several options to choose from.

In some cases, term deposits such as CDs or IRAs are great ways to save money, but they limit the accountholder’s access to their funds with early withdrawal penalties. For customers who don’t want their savings to carry those kinds of limitations, most banks offer a couple of more flexible savings options: savings accounts and money market accounts.

When you’re looking for a savings option, you probably have a number of questions. One of the questions we hear more often is, “What’s the difference between a money market account and a savings account?”

This month, we’re answering that question and a few others as we explore the choice: money markets vs. savings accounts.

What Is a Savings Account?

Generally speaking, a savings account at a bank is a special type of account that allows you to deposit money, earn a low or moderate amount of interest on your deposits, and have access to your cash within some basic limitations.

Specific accounts may vary in the amount of interest paid, withdrawal limitations, and features offered. Some savings accounts don’t pay interest or require a minimum balance to earn interest. Most will come with an ATM card that allows you to deposit to or withdraw from the account at an automatic teller.

In most cases, savings accounts have the lowest transaction limits of a bank’s standard deposit accounts, allowing only a few withdrawals a month before assessing additional fees. They also typically have some of a bank’s lowest account minimums, meaning that they’re an excellent option for customers who are just starting out with savings or who are only planning to use the account to save up for a small or moderate purchase.

What Is a Money Market Account?

Money market accounts are a more flexible option for savings. They allow for easier access to money and usually a higher interest rate, but they require larger minimum balances.

Money markets usually offer checks in addition to ATM cards. That doesn’t mean that money markets are a substitute for a checking account, however – money markets are geared towards savings, and attempting to use the account as a day-to-day repository will almost certainly result in paying additional fees each month as you exceed the transaction cap. For example, our Bank of Dudley money market accounts have a cap of six withdrawals per month; any withdrawals over six will impose a $3 fee.

Most banks’ money markets carry the same or a higher transaction cap as the bank’s savings accounts.

Money markets also usually pay more interest than a comparable savings account, but that’s not always the case. Before choosing an account, you should always check the bank’s current yield rates to see which account type will work best for you.

Why Is It Called a Money Market Account?

Money market accounts are so named because the interest rate accountholders earn with these accounts is based on the short-term debt investment trading market, commonly called the “money market.” The overall money market interest rate is usually higher than the rate used to set other deposit account interest rates.

Money Market vs. Savings Accounts: Security

If you choose an FDIC member bank as your financial partner, that bank’s savings and money market accounts will both be covered under FDIC deposit insurance. (Read last month’s article for a discussion of how FDIC deposit insurance protects)

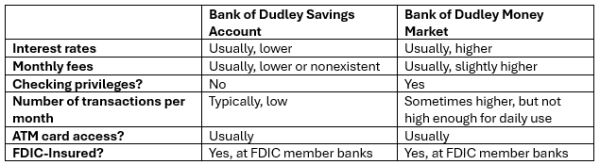

Money Market vs. Savings Accounts: Overview

If you’re still wondering which account type is right for you, we’ve assembled this table to help you understand some of the differences at a glance:

Which Account Type Is Right for You?

While both account types can be beneficial for folks looking to save money, each has its unique strengths that make it better for specific customers. The absolute best way to decide which account type is right for you is to talk to the trusted professionals at your local bank. But if you want some information to help start the conversation, here are some general use cases:

Savings Accounts

With lower fees and minimum balances, savings accounts are good starting places for accountholders who are just beginning their savings journey. Low transaction caps and limitations on account access are helpful for those who need a little extra incentive to keep their hands off of their savings. In some cases, special offers or unusual market conditions can cause some high-yield savings accounts to yield more interest than a bank’s money market offerings.

Money Market Accounts

Usually featuring higher opening balances, money markets are generally a better option for accountholders who already have a reasonable amount of savings. Additional access options like checks and debit cards make money markets attractive for people who often need to spend directly from their savings. And, of course, the usually higher interest rates are appealing to those who want to maximize their return on their deposited savings.

FDIC-Insured, Customer Focused, and 100% Local: Bank of Dudley

Since 1905, the team at Bank of Dudley has remained dedicated to helping our neighbors find financial success. Our local bankers are always ready to help you navigate the complex world of personal and business banking, and we’re 100% committed to helping you find the products and services that work for you – and helping you meet your financial goals.

Call today and discover true relationship banking: 478-277-1500